Managing personal finances can seem like a complex task, especially if you believe that making money last means cutting out all your moments of leisure. However, the secret to a healthy financial life is not total deprivation, but balance. That is exactly where the 50/30/20 Rule comes in—one of the most practical and effective financial planning methods in the world.

Whether you have multiple streams of income, a flexible revenue, or simply want to take definitive control of your monthly budget, this step-by-step guide will show you how to apply this methodology to your routine today.

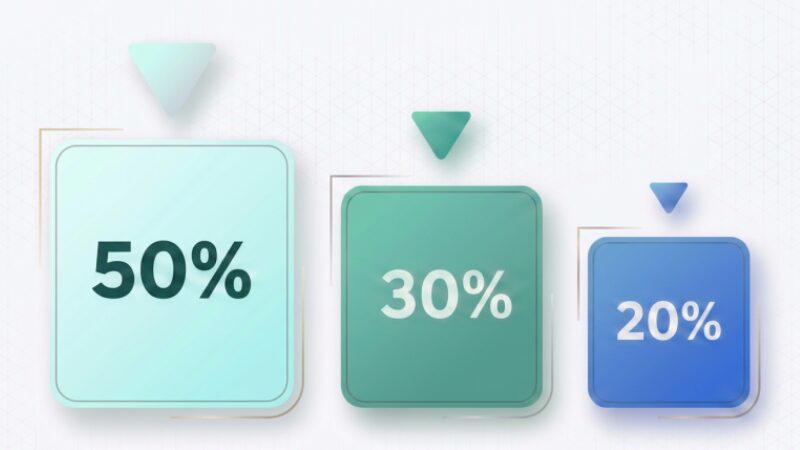

What is the 50/30/20 Rule and Why Does It Work?

Created by financial expert and Harvard professor Elizabeth Warren, the 50/30/20 Rule is a budget-splitting method that divides your monthly net income into three major categories: Needs, Wants, and Financial Priorities (Savings/Debt).

The main advantage of this model is its simplicity. Instead of tracking hundreds of tiny categories in a rigid spreadsheet (like separating bakery expenses, afternoon coffee, and parking), you focus on three large unified buckets. This brings mental clarity and makes the habit of managing money sustainable in the long run.

How to Divide Your Income in Practice (Step-by-Step)

To start applying the technique, the first step is to calculate your net monthly income. If you receive a fixed salary, it is the amount that hits your account after tax deductions. If you are self-employed or have variable income, take an average of your last three months.

Once you have the total amount, divide it according to the percentages below:

50% for Needs (What is essential) Half of everything you earn must be strictly allocated to the fundamental expenses for your survival and daily maintenance. If you stop paying any of these bills, your life will be directly affected.

This category includes:

- Rent, mortgage, or HOA fees;

- Utility bills (water, electricity, internet, and gas);

- Groceries and basic food;

- Transportation (gas, car insurance, maintenance, or public transit);

- Health insurance and essential medications.

Pro Tip: If your basic needs are consuming more than 50% of your current income, it is a warning sign that your cost of living is too high for your current financial level.

30% for Wants (Your lifestyle) This is where most traditional planning fails and the 50/30/20 Rule shines. You should not eliminate your fun. This category is dedicated to expenses that bring quality of life and satisfaction, but that could be cut in an emergency situation.

This category includes:

- Dining out and weekend delivery;

- Streaming service subscriptions and apps;

- Clothes, shoes, and accessories (not urgently needed);

- Travel, movie tickets, and hobbies;

- Personal care and aesthetics.

Keeping this bucket at 30% ensures you stay motivated to work and produce, knowing that your effort also translates into immediate, organized rewards.

20% for the Future (Savings and Debt Paydown) The last 20% of your monthly budget is the most critical for your long-term stability and wealth building. This money should be set aside right at the beginning of the month, aimed at protecting your future.

This category includes:

- Building your Emergency Fund: The first and most important pillar of asset protection;

- Investments focused on retirement or financial freedom;

- Paying off or amortizing structural debts (such as high-interest credit cards or loans).

Common Mistakes When Applying the Method and How to Avoid Them

Although the theory is simple, in practice some slips can disrupt your budget. The most common mistake is disguising wants as needs. For example: eating is a need, but dining at an expensive restaurant on Saturday is a want. Be extremely honest with your entries.

Another vital point is consistency. If your needs spike to 55% in one month, try to compensate by reducing your wants to 25% the following month, keeping the 20% for your future completely untouched.

Taking the Next Step in Your Financial Protection

The 50/30/20 Rule is the perfect foundation for organizing the money that comes in, but true financial planning goes further: it requires shielding. It is no use perfectly organizing your 50% of needs if a health or work emergency compromises your entire family income overnight.

If you live in the Massachusetts area and want to structure a personalized plan to protect your assets, accelerate your emergency fund, or understand the best insurance mechanisms to shield your current wealth, the support of a licensed specialist makes all the difference.

Want to take the next step and build a bulletproof financial strategy for your reality? Schedule a personalized consultation with Leandro Santiago and get your free financial assessment today.